Introduction: Why Good Businesses Still Get Rejected

In the booming economic landscape of 2025, India has over 7.8 crore business entities, of which MSMEs cover the major portion not only in GDP but also in the employment sector. As of November 2025, 7.16 crore (71.6 million) MSMEs are registered on the Udyam Registration Portal and Udyam Assist Platform (UAP), but still, only about 14% of MSMEs have access to formal institutional credit, meaning the vast majority, nearly 86%, remain outside the formal lending ecosystem. Among those who do apply, post-pandemic data indicates rejection rates of 40–50% for formal bank applications, a pattern that continues to weigh on MSME credit access today.

Even as MSME credit's share in total bank lending reached an all-time high of 17.7% in May 2025, with outstanding loans exceeding ₹14.3 lakh crore, this remains far below the 37% to 50% share that MSMEs command in developed economies, underscoring a deep structural gap in India's credit ecosystem.

But why are business loans getting rejected? The primary hurdle for most entrepreneurs is the lack of collateral for business loan approval. Standard institutional lenders typically follow a "safety-first" approach, prioritising tangible assets over operational success. When a loan is rejected due to collateral issues, it highlights a structural gap in the market: the heavy reliance on collateral for business loan security.

Understanding the shift between a secured vs unsecured loan India is vital for any business owner. While traditional banks demand property or gold, the modern financial ecosystem is evolving to recognise that rejection is often a structural mismatch, not a failure.

What “Lack of Collateral” Really Means

A collateral for business loan refers to an asset, such as property, equipment, or gold, that a company offers to a lender as a guarantee. If the firm cannot repay the debt, the lender can take the asset to recover the money.

Simply, collateral means an asset that a borrower (the business) offers to a lender (the bank) as security for a loan (business loan).

For many small business owners, a business loan rejection India happens simply because the enterprise does not own enough high-value assets to meet bank requirements. Also, the requirement of collateral for a loan varies bank to bank and loan to loan, as banks see what amount is demanded and the borrower’s creditworthiness.

But, still, the majority of traditional banks debate between a secured and an unsecured loan India model. In a secured loan, the bank feels safe because there is a physical backup. In contrast, an unsecured loan relies only on the company’s reputation and credit history. From the lender’s perspective, the risk perception in the Indian market is quite high, but if we look from the borrowers’ perspective, then a traditional loan is a loss, as the borrower will get only 60-70% of the valuation of the collateral.

That’s why a loan rejected due to collateral is so common in India. Asset-backed lending is the standard because it provides a "safety net" for the bank. However, the lack of collateral for business loan applications does not mean the company is failing; it just means the firm does not fit the traditional "risk-free" system.

If a business wants to raise a higher amount with the same collateral, then it should connect with professionals, like Assets2Loan services. Here, the business can raise a 2x or more valuation of the asset without giving much risk, as these kinds of professional platforms make a lender connect with the asset owner directly without any mediator and help them raise more funds for their businesses.

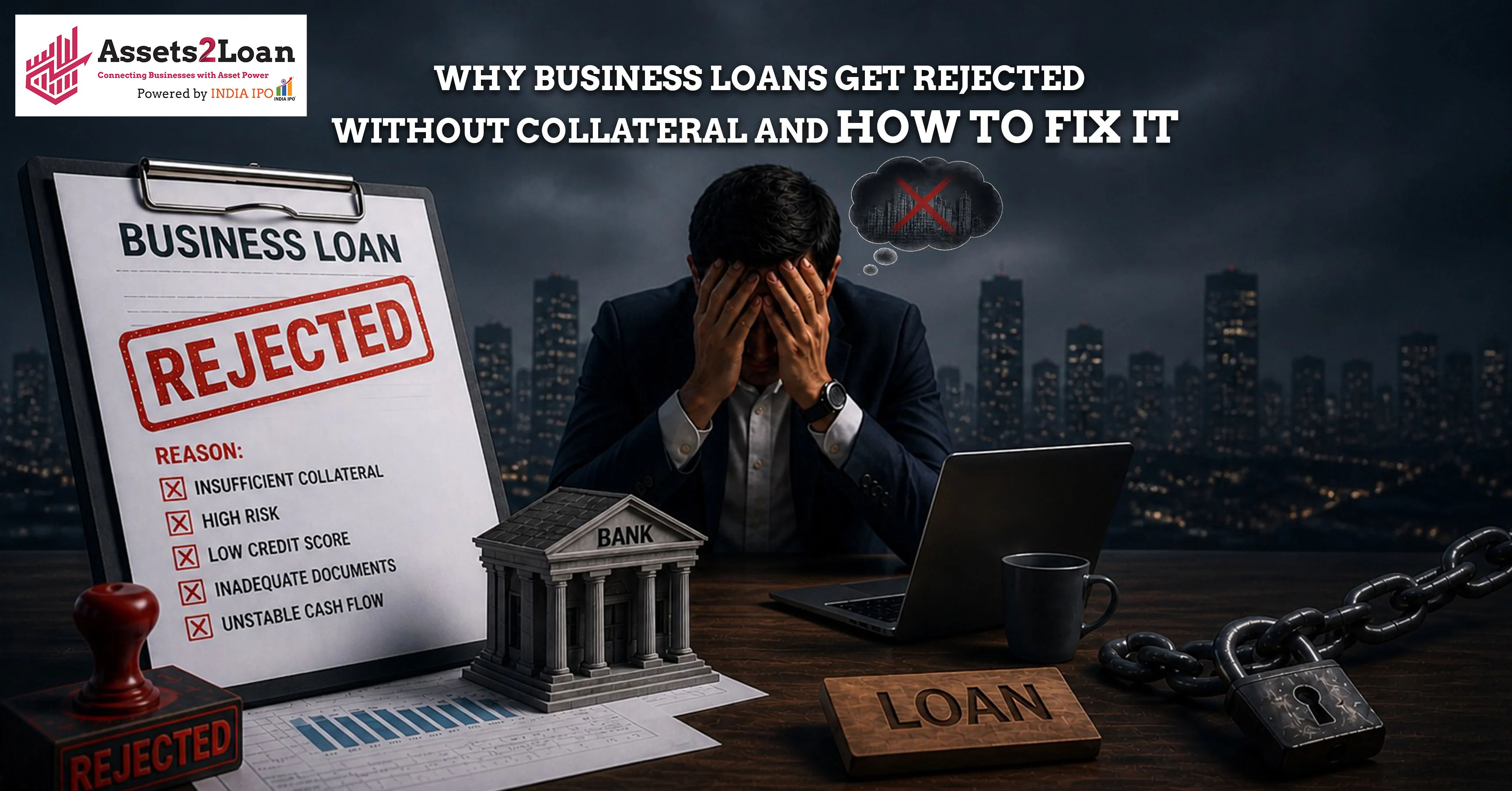

Why Your Loan Was Rejected

A business loan rejection in India often happens for certain reasons, like when the lender thinks that you are not able to pay back the loan within the time, or the borrower’s given collateral is not strong enough to provide the demanded valuation and so on. Let’s understand the top reasons that make a loan rejected within seconds of opening a business loan file:

A. No Tangible Security

The most common reason for a loan rejection is due to a lack of collateral, which means the absence of enough physical assets to get loan approval in India. As per the industry data, during the post-pandemic period, nearly 40% to 50% of MSME loan applications were rejected by formal banks, with 'lack of collateral' cited as the primary reason in 60% of those rejections — a pattern that continues to affect formal credit access today. This traditional method of loan approval has become a major roadblock for growing companies in India.

B. Weak Collateral Structure

Sometimes, a company possesses assets, but the collateral for business loan requirements is not met because the assets are already pledged elsewhere or have low resale value. If a firm's assets are deemed "unusable" by the bank's valuation standards, the application may still face rejection despite the business having some physical backing.

C. Credit vs Collateral Gap

A common misconception is that a strong CIBIL MSME Rank (CMR) alone ensures funding. While a good score is helpful, there is often a gap between creditworthiness and security requirements. A business may have a perfect repayment history, but if there is a lack of collateral for business loan backing, the lender may still view the request as too risky.

D. Risk-Based Lending Models

This model determines loan interest rates and terms by analysing a borrower's specific risk profile, charging lower rates to lower-risk borrowers and higher rates to higher-risk ones.

The Indian lending ecosystem heavily prioritises secured loans over unsecured loans. Banks use risk-based models that favour asset-backed lending to protect their capital. And those are common reasons for rejection of loans in India, but any business that wants to raise capital should connect with a professional advisor to ease their funding procedure, like Assets2Loan, which helps in providing funding with full security, maintains transparency and efficient processes.

The Reality of Collateral-Free Loans in India

The scenario of lending without collateral in India has changed dramatically due to technological advancement and inclusion in finance. While these loans offer immediate liquidity without asset security, the reality involves a complex balance of high interest rates and stringent credit assessments. Understanding this mechanism is essential for any company navigating the modern domestic credit ecosystem effectively.

- Limited Availability: Most financial institutions still maintain a conservative stance. A company may find that a business loan rejection India is still possible if the firm's cash flow does not meet strict eligibility criteria.

- Smaller Ticket Sizes: Unsecured loans typically offer smaller amounts. These are often capped at lower limits unless the debt is backed by specific government guarantee frameworks.

- Higher Interest Rates: Because the lender takes on higher risk without physical security, a firm should expect increased borrowing costs. This is a direct consequence of the lack of collateral for business loan applications, where the "risk premium" is passed to the business.

- Dependency on Schemes: Most banks only offer an MSME loan without collateral by leveraging the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE).

In India, if a firm wants to get its loan approved, it should work on its financials and collateral, as banks still support collateral-based loans, even though they offer a valuation of 60-70% of the collateral. Between January and November 2025 alone, CGTMSE approved guarantees worth ₹3.77 lakh crore, having also crossed the milestone of one crore cumulative guarantees since inception.

What to Do After Loan Rejection

If a business loan gets rejected, still, a business loan rejection in India can be a setback, but it serves as a critical analysis tool for a company. Here are some points that need to be taken care of after a loan rejection:

- Improve Credit Profile: A firm must regularly monitor its business credit score, mainly in collateral cases. For business borrowers, lenders assess the CIBIL MSME Rank (CMR), not the personal CIBIL score. A CMR of 1 to 3 indicates the lowest credit risk and qualifies the firm for the most competitive interest rates and faster approvals.

- Strengthen Financial Documentation: Banks (lenders) will demand proof of cash flow when collateral is required for business loan approval. A company needs to have its GST returns up-to-date, an audited balance sheet, and bank statements as proof that the organisation can handle debt without any tangible assets.

- Reduce Existing Debt: Normally, a debt-to-income ratio determines the reason for rejection of a business loan application. By paying down current liabilities, a company improves its debt-service coverage ratio. An ideal Debt-Service Coverage Ratio (DSCR) is generally considered to be 1.25 or more.

A business loan rejection is not a final result but a signal for a firm to recalibrate. With nearly 28% of MSME applications in India currently facing rejections due to preventable documentation gaps or financial visibility issues, shifting to digital reconciliation is key. Improving the firm's CIBIL MSME Rank to CMR 1–3 and leveraging platforms like PSB Loans in 59 Minutes can transform a firm's future funding prospects.

The Real Fix: Move from Credit-Based to Asset-Based Funding

Indian loans have been predominantly credit-based, wherein the income stream of the borrower, along with his credit score and other financial documents, is of utmost importance. But when we talk about India, which has more than 7.16 crore MSMEs registered, this method has led to a credit shortage of ₹25-30 lakh crore. The actual solution to the business environment of India is transitioning from credit-based to asset-based financing, where the value of the asset becomes the trust factor where the balance sheet fails.

In a credit-heavy model, a firm is often judged by its CIBIL MSME rank or two years of stable ITRs, requirements that many growing Indian firms cannot meet. In contrast, asset-based financing shifts the focus to what the company owns. In India, an asset-based shift example is the Trade Receivables Discounting System (TReDS), which saw a massive surge in FY24, processing over ₹2 lakh crore in invoices. By treating an unpaid invoice as a liquid asset, firms can secure immediate capital at rates averaging around 8%, significantly lower than the 18–24% typical of unsecured business loans.

The Strategic Advantage

This shift is transformative for several reasons:

- Lower Cost of Capital: Asset-based funding is usually considered less risky by banks, which results in lower borrowing costs than those charged for unsecured loans.

- Higher Funding Limits: While credit limits are tied to monthly earnings, asset-based lending is tied to the liquidation value of the collateral, often unlocking much larger pools of capital for expansion.

- Resilience in Volatility: During market downturns, income can fluctuate. However, the underlying value of tangible assets remains more stable, providing a safety net that keeps credit lines open when the business needs them most.

Ultimately, assets create a "collateralised trust." When lenders focus on the recoverable value of an asset rather than just the volatility of monthly income, they reduce the risk of Non-Performing Assets (NPAs). For the Indian entrepreneur, this transition means that growth is no longer capped by a credit score but fueled by the actual value held within the firm.

How Asset-Backed Financing Solves Collateral Problems

For many growing businesses in India, the lack of "liquid" capital often stalls ambitious expansion plans. Traditional lending frequently traps these firms in a cycle of high interest and low limits. However, Asset-Backed Financing (ABF) offers a structural solution by converting idle physical wealth, such as land, commercial property, or industrial equipment, into active funding support.

By shifting the focus from the borrower’s current cash flow to the underlying value of the security, ABF effectively solves the "collateral gap." This model enables 3 critical advantages:

- Higher Loan Amounts: Since the loan is anchored to the market value of the asset rather than just monthly profit margins, companies can access significantly larger pools of capital.

- Lower Interest Rates: Asset-based loans are considered relatively less risky by lenders, who can be assured of getting their recovery via collateral. This security allows the firm to negotiate more competitive, "prime" interest rates compared to unsecured credit.

- Longer Repayment Tenures: Unlike short-term working capital loans, ABF structures often allow for extended tenures, aligning the repayment schedule with the long-term lifecycle of the asset being leveraged.

The success of these loans relies on 3 pillars: Asset Value, Clear Title and Marketability. Lenders conduct strict due diligence to ensure the property is free of legal encumbrances and can be easily liquidated if necessary. By unlocking the value trapped in their balance sheets, companies can transform their "dead" assets into the fuel required for their next phase of industrial or commercial growth.

What If You Don’t Have Collateral?

For many ambitious business owners in India, the traditional banking conversation ends the moment the word "collateral" is mentioned. In a landscape where nearly 90% of enterprises are small or mid-sized, the reality is that most firms do not own sprawling commercial real estate or ancestral land to pledge as security. If your business operates out of a rented office or relies on intangible intellectual property, the "No Collateral, No Loan" policy feels like an invisible ceiling on your growth.

However, the "collateral gap" doesn't have to be a dead end. The modern financial fix involves moving beyond what the company currently owns to what it can strategically access. One powerful solution is Third-Party Collateral, as it allows a firm to secure a loan by using assets owned by someone else, be it a director, a dedicated investor, or a specialised partner who believes in the company’s cash flow and is willing to pledge their property to back the debt.

Further evolving this concept are Structured Collateral Partnerships. Instead of struggling alone, a company can enter into a formal agreement with an asset-holding entity. This creates a "collateralised trust" where the lender sees a secured asset and the business owner gets the capital they need to scale.

This is exactly where Assets2Loan bridges the divide, a professional advisory that understands that while a firm might lack a deed in its name, it possesses the vision and revenue to thrive. They connect capital-desire businesses directly with verified landowners and asset-heavy partners looking for productive ways to leverage their holdings. By facilitating these "Asset-to-Business" matches, they ensure that a lack of personal property never stands in the way of a company’s potential. You bring the business; Assets2Loan help you find the security to fund it.

Types of Assets That Can Be Used for Business Loans

Selecting the appropriate collateral is a critical step in optimising a firm’s borrowing capacity. Not all assets are viewed equally by financial institutions; the loan-to-value (LTV) ratio, interest rates and approval speeds vary significantly depending on the nature of the security provided. Understanding the specific categories of eligible assets allows the business to strategically leverage its balance sheet.

The following asset types are the most commonly accepted for securing institutional business loans:

1. Residential Property

Self-occupied or rented residential units, such as apartments, bungalows, or penthouses, are highly favoured by lenders. Due to the high liquidity and consistent market demand for residential real estate, these assets often command the lowest interest rates. The firm can typically secure a loan of up to 60%–75% of the property’s market value. However, the property must be located within municipal limits and possess a clear, marketable title.

2. Commercial Property

Business-owned assets can be utilised to unlock significant growth capital. Even though the rate of interest on the loans for commercial properties may be marginally higher compared to the rate charged for loans against residential properties, they have their own strengths: the size of the loans is larger, owing to the high-value property that serves as collateral. Lenders focus heavily on the property's location and its potential to generate rental income as an additional layer of security.

3. Land (Non-Agricultural)

Raw land or industrial plots can be leveraged, though they come with specific conditions. Most institutional lenders avoid agricultural land due to complex legal restrictions. However, non-agricultural (NA) land, commercial plots, or industrial land are widely accepted. Because land is considered a less "liquid" asset than a constructed building, the LTV ratio is usually more conservative, typically ranging between 40% and 50%.

By identifying which assets are available, whether owned directly by the company or accessed through a structured third-party partnership, the business can ensure it secures the most cost-effective and scalable funding solution.

Loan vs Asset-Backed Structuring (Strategic Comparison)

Choosing the right financing path is a defining moment for any Indian enterprise. Whereas the traditional loan process is not “alien” to many people, how such a process can be structured is the determining factor for whether it will turn out to be successful or end up in the lender's bin. With 2026 being an era of caution in the lending industry, it is important to grasp these aspects.

The Unsecured Loan Perspective

For service-oriented or asset-light firms, the unsecured business loan is the default choice. From the lender’s perspective, this is a "pure trust" play, because there is no collateral to seize in case of default; the bank or NBFC relies entirely on the business's CIBIL MSME Rank (ideally CMR 1–3, indicating low-to-negligible default probability) and Debt Service Coverage Ratio (DSCR) (ideally 1.25 or higher).

While these offer speed, they come with a higher rejection rate (estimated at 25–30%) and punishing interest rates, often ranging from 16% to 24%. For the business owner, this approach feels like a constant uphill battle to prove worthiness through paperwork alone.

The Traditional Bank Loan Perspective

Standard bank loans often sit in a middle ground, requiring a mix of strong financial "vintage" (usually 3+ years) and high turnover. Lenders here are looking for stability and "safety first." They demand rigorous documentation, from audited ITRs to GST compliance records.

This often leads to a "Strict Approval" cycle. Even with good revenue, a firm might be rejected if its industry is deemed "high-risk" or if its cash flow shows even slight seasonality.

The Asset-Backed Structuring Perspective

In asset-backed structuring, the lender asks, "What value can we secure?" By tying the loan to a physical asset such as machinery, gold, or commercial property, the lender's risk is mathematically reduced.

This perspective leads to significantly higher approval chances. In fact, secured loans in India typically see interest rates 3–7% lower than unsecured counterparts. For a firm, this isn't just a loan; it’s a strategic use of the balance sheet to manufacture trust.

In the Indian market, collateral is the ultimate "risk-mitigator." Moving from a credit-based to an asset-backed mindset doesn't just lower the interest costs; it opens doors that were previously locked by a simple credit score.

Common Mistakes That Lead to Rejection

Even with a strong business model, the path to institutional funding is often hindered by avoidable procedural errors. Understanding why applications fail is the first step toward securing a successful mandate. For most firms, rejection is rarely a reflection of the business's potential but rather a result of poor financial engineering, as many firms fail because their Debt Service Coverage Ratio (DSCR) is below 1.25 or due to poor documentation.

To ensure the company’s application remains viable, the management must avoid these four common pitfalls:

- Applying Without Adequate Collateral: Relying solely on cash flow is a high-risk strategy. In the current regulatory environment, lenders are increasingly hesitant to provide large-scale capital without tangible security. Attempting to secure substantial funding without a collateral plan often leads to immediate disqualification.

- Ignoring Asset Structuring: Many firms fail because they do not "package" their assets correctly. Effective structuring involves more than just offering property; it requires aligning the asset’s value, title clarity and marketability with the specific requirements of the loan. Ignoring these nuances can lead to a valuation gap that stalls the entire process.

- Poor Documentation: Trust depends upon transparency in the banking industry. Any inadequacies in accounting records, legal issues affecting property ownership, or outdated audit reports indicate deficiencies in professional governance. All representations in the proposal must be substantiated with solid evidence.

- Wrong Lender Targeting: Not every financial institution has the appetite for every type of asset. Business owners often apply to Tier-1 private banks when their profile is better suited for NBFCs (non-banking financial companies) or small finance banks (SFBs).

SFBs in India recorded over 20% year-on-year loan portfolio growth in FY26, significantly outpacing the broader banking sector's 13.8% average credit expansion, largely driven by their more flexible collateral-lite underwriting policies for micro-enterprises.

By addressing these factors early, the firm transitions from a "borrower in need" to a "strategic partner." By not making such mistakes, a company ensures the proposal is received with the proper professionalism it deserves.

Who Should Consider Asset-Backed Funding?

The asset-backed funding approach is not a universal solution; however, for certain types of businesses, it is the best method for obtaining significant capital investment. It is necessary to establish whether the business belongs to this category in order to ascertain whether the financial approach will produce the desired ROI.

The following entities should prioritise asset-backed structures over traditional credit lines:

1. MSMEs with Aggressive Growth Plans

For MSMEs, there is usually a “growth trap,” where, despite having enough orders from the market, they do not have enough liquid cash flow to expand their business. In such circumstances, the utilisation of the available assets that the firm owns, as collateral, will enable it to access the significant funds required for various activities.

2. Businesses Facing Institutional Rejection

It is common for high-potential firms to be rejected by traditional banks due to "technicalities," such as a brief dip in historical profitability or a lack of long-term credit seasoning. Asset-backed funding provides a "Real Fix" here; by offering tangible security, the business shifts the lender's focus from past financial hiccups to the current, measurable value of the collateral, significantly increasing the chances of approval.

3. Promoters with Access to Land or Non-Core Assets

Many promoters hold significant personal or family wealth in the form of real estate that remains idle. Strategically pledging these non-core assets to fund the company’s expansion is a hallmark of sophisticated financial planning. This allows the firm to access "cheaper" money (lower interest rates) compared to the high cost of equity dilution or unsecured debt.

4. Expansion-Stage Companies

Firms moving from a local to a national or international presence require a stable, long-term capital base. Expansion involves high upfront costs with delayed returns. Asset-backed loans, with their longer repayment tenures and higher ticket sizes, provide the necessary runway for the company to achieve its new milestones without the constant pressure of short-term liquidity crunches.

|

Metric |

Unsecured Loan |

Asset-Backed Funding |

|

Avg. Interest Rate |

18% – 26% |

9% – 14% |

|

Processing Time |

48 Hours – 7 Days |

10 Days – 21 Days |

|

Max Loan Tenure |

3 Years |

Up to 10–15 Years (Real Estate backed) |

|

Primary Rejection Reason |

Low CMR / Cashflow |

Low Asset Valuation / Title Issues |

Ultimately, any firm that possesses or can access through partnerships tangible assets should consider this route. It transforms a static balance sheet into a dynamic engine for growth, ensuring that the company’s vision is never limited by its current cash flow.

Conclusion: Loan Rejection is a Structuring Problem

Rejection of a business loan due to collateral often starts from the management of the business; a loan rejection is not a verdict on the company’s potential or the weakness of its business model; rather, it is a symptom of a structuring problem. When a firm relies solely on its income statement to prove its worth, it invites the highest level of lender scrutiny and risk assessment.

The transition from a rejected application to a successful mandate lies in how the capital is structured. By pivoting from credit-based requests to asset-backed funding, the business fundamentally changes the conversation. Assets create an "equity of trust"—they provide a tangible guarantee that mitigates the lender's fear of default.

Ultimately, the goal for any ambitious firm is to ensure its financial architecture is as strong as its operational strategy. When credit history fails to tell the full story, assets unlock the door. By leveraging tangible security, the company moves past the limitations of its cash flow and gains the institutional support necessary to achieve its long-term strategic objectives.

Rejection is just a signal to reorganise, not to give up!

FAQs

- Why was my business loan rejected due to a lack of collateral?

Lenders prioritise risk mitigation. Without tangible security, a bank’s only recourse is the company's cash flow. If the firm’s income history is deemed insufficient or volatile, the perceived risk becomes too high for institutional mandates, leading to an immediate rejection despite a strong business model.

- Can I get a business loan without collateral in India?

Yes, via unsecured business loans or government schemes like CGTMSE. However, these typically carry significantly higher interest rates, offer lower capital limits and involve stringent eligibility criteria regarding the company’s vintage and monthly turnover, which may not support large-scale expansion.

- What assets can be used for business loans?

Acceptable assets include residential houses, commercial office spaces, industrial sheds and non-agricultural land. Additionally, high-value machinery or liquid securities like fixed deposits and gold can be leveraged. The asset must possess a clear, marketable title and be free from existing legal encumbrances.

- How can I improve my business loan approval chances?

The best approach to pivot is for the corporation to move towards the asset-based model. Good corporate governance, auditable financial records, and a good balance between debt and equity will serve to boost lender confidence. Identifying the proper financial institution familiar with the industry of the firm is also essential.

- What is asset-backed financing?

Asset-backed financing is a strategic lending model where the loan is secured by the company’s physical or financial assets. This structure allows the firm to access larger capital pools and lower interest rates, as the collateral provides the lender with a guaranteed secondary source of repayment.

- What can I do after a business loan rejection?

Management should first identify the specific "rejection code." If the issue is a lack of security, the firm should consider restructuring the request using third-party collateral or platforms like Assets2Loan. Transitioning from an unsecured to a secured application often turns a "no" into a "yes."